SME Digital Finance and Payments Behaviours: Southeast Asia Report 2023

Welcome to this comprehensive industry report, one that unveils the intricate tapestry of lending and payments behaviours exhibited by the vibrant community of small and medium-sized enterprises (SMEs) across Southeast Asia. Delve deep into the fabric of the financial ecosystem that shapes the economic backbone of our region.

Learn about Southeast Asia's SMEs:

-

What they spend on

-

How they send and receive payments

-

How they secure funding

-

Their financing needs and insights into spending seasonality

-

Their overall business outlook

About The Study

We wanted to understand what kind of challenges micro, small, and medium enterprises are facing and how they’re using digital financing and payments to capture business opportunities and efficiencies.

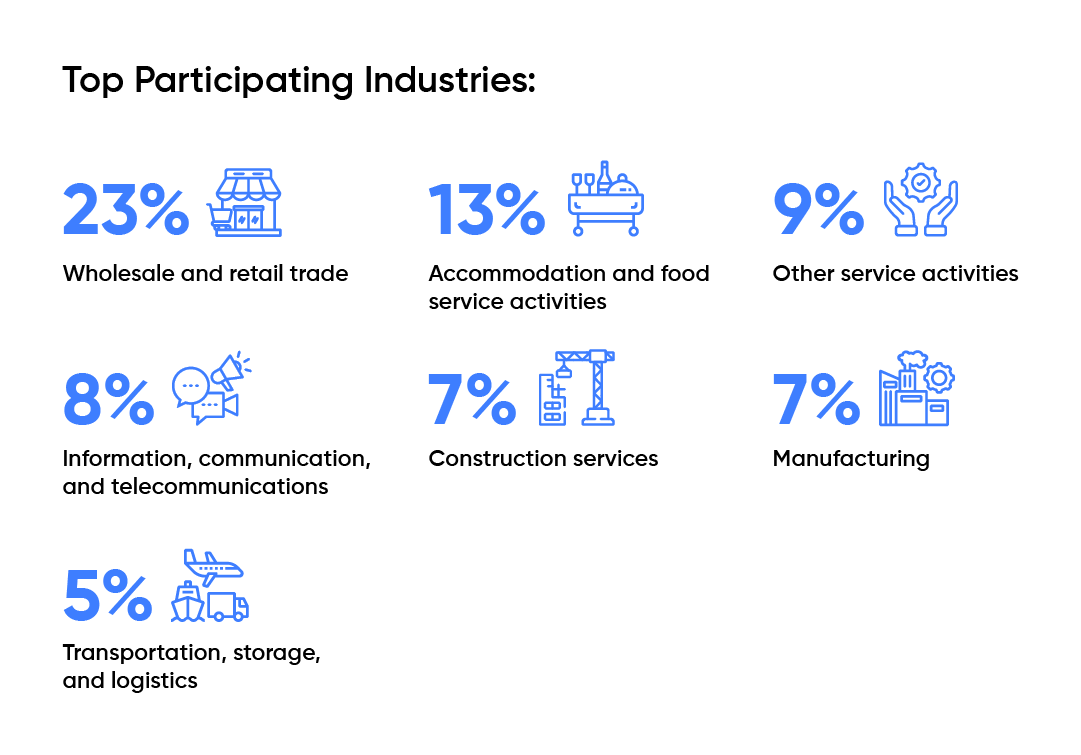

To find out, we surveyed 977 SMEs in Indonesia, Malaysia, Singapore, Vietnam, and Thailand from across several industries. Most respondents fall under the micro SME category (74%) and are the business owners themselves (63%).

To find out, we surveyed 977 SMEs in Indonesia, Malaysia, Singapore, Vietnam, and Thailand from across several industries. Most respondents fall under the micro SME category (74%) and are the business owners themselves (63%).

Continue reading for more highlights or download the full report.

Keen, Yet Cautious: SMEs Struggle With Financial Access in Southeast Asia

Across Southeast Asia, both traditional and digital financial companies have been creating innovative products and services for small and medium enterprises (SMEs). But an abundance of choice does not necessarily lead to greater ease in accessing finance. SMEs consider different factors and tradeoffs when choosing financial solutions.

These choices can inadvertently deter financing flexibility, especially when SMEs don’t get enough information, guidance, and support in choosing products like funding schemes, SME business loans, and cloud-based software.

The results of our regional SME financing market research reflect such friction — while SMEs in Southeast Asia are actively searching for better financial products and trying out solutions offered by financial technology (FinTech) companies, many are also sticking to traditional methods like cheque payments and manual business processes.

To overcome these barriers, FinTech companies need to do more to foster trust with SMEs, facilitate better understanding of alternative financing options, and demonstrate the success of these programmes. SMEs’ piecemeal adoption of alternative finance — instead of a cohesive and systematic approach — also signals an opportunity for FinTechs to offer unified financing solutions to SMEs.

By giving SMEs the tools they need to strengthen cash flow and gain more credibility and leverage with their suppliers, financial companies can become trusted advisors that help sustain and grow SMEs, the lifeblood of the Southeast Asian economy.

The Way Forward for Southeast Asia’s SMEs: New Solutions for Old Problems

The Way Forward for Southeast Asia’s SMEs: New Solutions for Old Problems

Amidst Southeast Asia’s thriving digital economy and strong mobile internet access, SMEs continue to face financial challenges and are still in the early stages of digital finance.

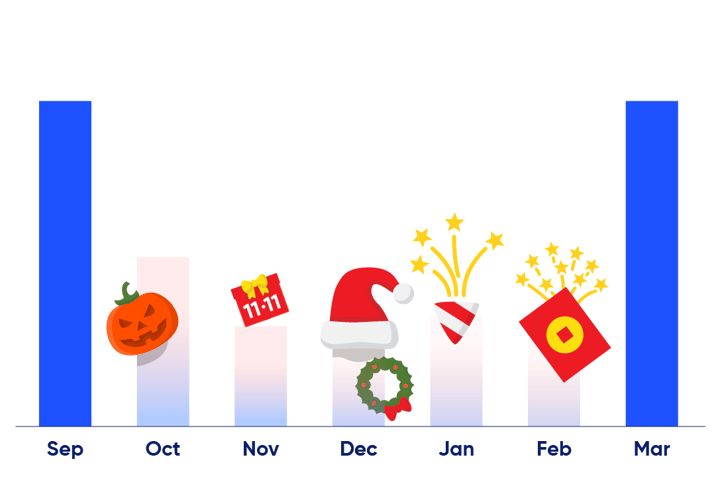

Our study found that cash flow remains a key SME concern, with many spending most of their funds to support daily operations and buy inventory and supplies, and worrying about paying suppliers and receiving payment from customers on time. These concerns are further aggravated by seasonal cash flow fluctuations when festive seasons increase consumer demand and raw material prices, and end-of-year objectives to complete ongoing projects and implement new ones call for an infusion of funds.

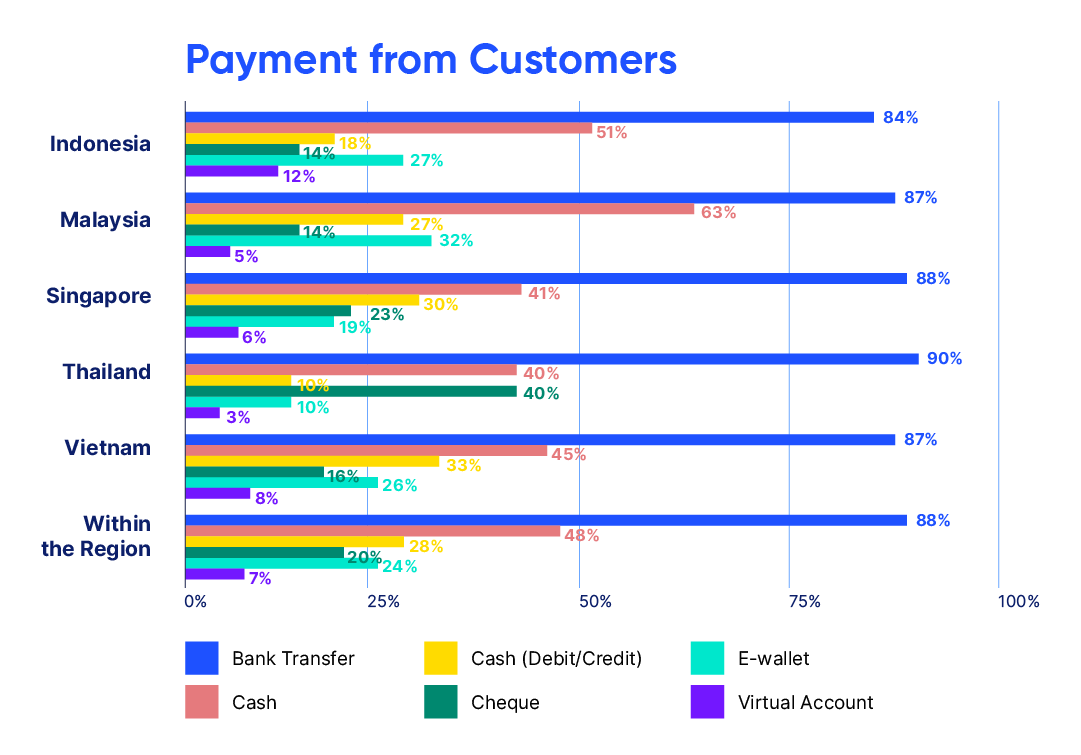

A vast majority still depend on banks to send and receive payments. Most SMEs’ transactions are also primarily local, with only a small portion doing cross-border transactions. And while many use accounting software to automate payment processes, there is a need for payment collection solutions — for both recurring, high-value transactions and mass payments — that would make the process easier and minimise late payments from customers.